- Air cargo volumes through UK airports climbed to 687,000 tonnes in Q3 2025, a modest year-on-year increase from 679,000 in the same quarter last year. But while quarterly performance was stable, cumulative figures for the year to date show cargo tonnage is trending below pre-pandemic highs.

According to the Civil Aviation Authority’s latest aviation trends data, the rolling annual cargo total reached 2.7 million tonnes by the end of Q3—flat compared to 2024, and down from the 2.8 million recorded in 2018 and 2017. Despite gradual recovery since 2020, when volumes dropped to 2.2 million, 2025 remains the weakest post-COVID year since 2021.

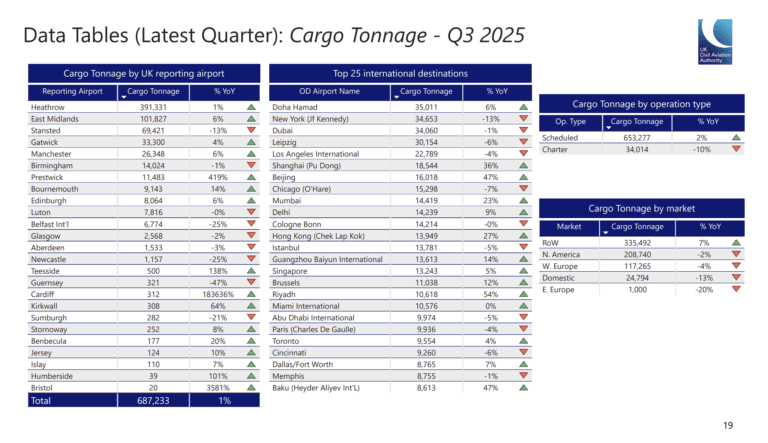

Heathrow retained its position as the UK’s top cargo hub, handling 391,331 tonnes in Q3—up just 1% year-on-year. East Midlands followed with 101,827 tonnes, growing 6%, while Stansted saw a notable decline of 13%, processing only 69,421 tonnes.

Prestwick posted the most dramatic increase of any reporting airport, up 419% to 11,483 tonnes. Cardiff also surged, albeit from a much lower base, registering a 1,836% jump to 312 tonnes.

Among carriers, Air China and China Southern Airlines were top performers, adding 11,000 and 7,000 tonnes respectively. In contrast, DHL Air and Federal Express each lost 4,000 tonnes, and British Airways declined by 6,000 tonnes.

The bulk of tonnage growth came from passenger aircraft bellyhold capacity, which increased by 7,000 tonnes year-on-year. Dedicated freighter services contributed an additional 2,000 tonnes. Scheduled cargo operations overall grew by 2%, while charter services fell 10%.

Markets outside Europe and North America—categorised as “Rest of World”—accounted for 335,492 tonnes in Q3, representing a 7% increase year-on-year. Domestic cargo, however, dropped 13%, and traffic to Eastern Europe was down 20%.

Top International Cargo Routes

The busiest international routes by tonnage were Doha (35,011 tonnes), JFK New York (34,653), and Dubai (34,060). While Doha and Dubai held steady, JFK traffic declined 13%. Other notable shifts included a 54% surge in tonnage to Riyadh and a 47% increase to Beijing.

While the Q3 uplift offers reassurance about the stability of the UK’s airfreight market, the broader annual trend highlights a sector still recalibrating. The 2025 quarterly performance—Q1: 653K, Q2: 684K, Q3: 687K—shows incremental improvement, but still lags behind the 705K tonnes recorded in Q4 2024.

The Civil Aviation Authority noted that nearly 700,000 tonnes were moved across the UK network between July and September, continuing a multi-year trend of moderate growth without major spikes.

As peak season approaches, all eyes are on whether Q4 can push annual tonnage closer to—or beyond—the 3 million mark. Much will depend on freight capacity during the winter holiday season, the pace of e-commerce flows, and how supply chains absorb wider macroeconomic and geopolitical shifts.